05/08/2016

Deciding to scrap your car can feel like a daunting task, particularly when you consider the intertwining complexities of vehicle insurance and official paperwork. Many vehicle owners find themselves grappling with questions about liability, responsibility, and the precise moment their obligations shift from them to the scrap company. This guide aims to demystify the entire process, providing clear, actionable advice on how to navigate the journey from an unrepairable vehicle to a properly scrapped one, ensuring you avoid pitfalls and manage your insurance effectively.

What Exactly is a Scrapped Car?

A car is typically deemed 'scrapped' when it has sustained such immense damage that it is beyond economical repair. Unlike vehicles that might simply need a new part or a bodywork repair, a scrapped car is fundamentally unfit to be on the road, often posing a significant safety hazard. In such instances, its value is primarily derived from the weight of its constituent materials – the metal frame, rubber from tyres, and other salvageable components. These vehicles are sent to an Authorised Treatment Facility (ATF), where they are depolluted and dismantled in an environmentally responsible manner, ensuring hazardous materials are disposed of correctly and valuable resources are recycled.

The Scrapping Process: A Step-by-Step Guide

Once you've decided that scrapping is the best course of action for your vehicle, following a structured approach will ensure a smooth and compliant process. Here’s a summary of the essential steps:

- Research Scrap Car Companies: Begin by searching online for reputable scrap car companies or Authorised Treatment Facilities (ATFs) in your area. Ensure they are legitimate and licensed.

- Obtain Multiple Quotes: Don't settle for the first offer. Contact several companies to get a few quotes. Prices can vary based on the vehicle's make, model, weight, and current metal prices, allowing you to find the best possible return.

- Accept the Best Quote & Arrange Collection: Once you've chosen a company, accept their quote and arrange a free collection of your scrap car. Most reputable ATFs offer this service at no extra charge.

- Provide Identification: On collection day, you'll need to provide identification to the scrap car dealer, such as a driving licence. This is a legal requirement to verify your ownership.

- Get a Receipt: Always ensure you receive a receipt from the scrap car dealer confirming the transaction. This is your proof that the vehicle has been handed over.

- Handle the V5C Registration Document: You must provide the scrap car dealer with your V5C registration document (log book). Crucially, you need to retain section 9 of the V5C document (or section 4 on V5Cs issued after April 2019).

- Notify the DVLA: Complete the section you retained from the V5C and send it to the DVLA. This is an absolutely critical step to inform the DVLA that your vehicle has been scrapped. Failure to do so can result in a fine of up to £1,000.

- Contact Your Insurance Company: As soon as your car has been collected and you've initiated the DVLA notification, inform your insurance provider. They will cancel your policy.

- Receive Your Certificate of Destruction (CoD): Within 7 days of your vehicle being scrapped by an ATF, you should receive an official Certificate of Destruction. This is definitive proof that your vehicle has been legally and properly disposed of.

How Scrapping Affects Your Car Insurance

The moment your car is scrapped, its status changes dramatically, and so too will its insurance requirements. A scrapped car is, by definition, no longer roadworthy and cannot be driven. This renders any existing car insurance policy for that specific vehicle redundant. Your insurer will see the car as having reached the end of its useful life, and therefore, it will no longer be covered under a standard policy.

Cancelling Your Insurance: Timing is Key

One of the most anxiety-inducing questions for many owners is whether to cancel their insurance before the car is even collected. The answer isn't always straightforward and depends on where your car is stored:

Scenario 1: Car Parked/Stored on the Road

If your car is currently parked or stored on a public road, even if it's undrivable or has been immobile for some time, it is a legal requirement in the UK to have an active insurance policy in place. In this scenario, the car remains your responsibility right up until the exact moment the scrap company collects it. The best course of action is to wait until the scrap company has taken the vehicle away before you officially cancel the policy. Reputable collection agents are typically covered by their own breakers yard insurance, so liability transfers at the point of collection.

Scenario 2: Car Stored on Your Private Property

If your car is kept entirely on your private property – whether it's on your driveway, in a garage, or elsewhere off the public road – there is no legal obligation for you to have insurance. However, this lack of insurance also means your vehicle would not be covered in the event of damage (accidental or criminal) or theft. While not directly related to insurance, you should inform the DVLA that your vehicle is off the road by completing a Statutory Off Road Notification (SORN). This is a quick and easy online process that stops you from having to pay vehicle tax and can result in a refund for any advance tax payments. Even without a legal obligation, some owners choose to consult their insurance provider before cancelling, especially if they have a significant no-claims bonus they wish to protect.

Here’s a quick comparison of insurance requirements:

| Storage Location | Insurance Legally Required Before Scrapping? | DVLA Notification (SORN) Recommended? |

|---|---|---|

| On Public Road | Yes (until collected) | No (unless moved off-road first) |

| On Private Property | No | Yes (to avoid tax/penalties) |

Notifying Your Insurer After Collection

As soon as your car is picked up to be scrapped, and you have completed and returned the relevant V5C slip to the DVLA, you must inform your insurer. Since your vehicle is no longer registered for public use, the insurer will cancel your policy. They will then advise you on whether you are eligible for a refund for any unused months of your premium or if your policy can be transferred to a new vehicle. Always ensure you get written confirmation from your insurer that your policy has been cancelled for your records.

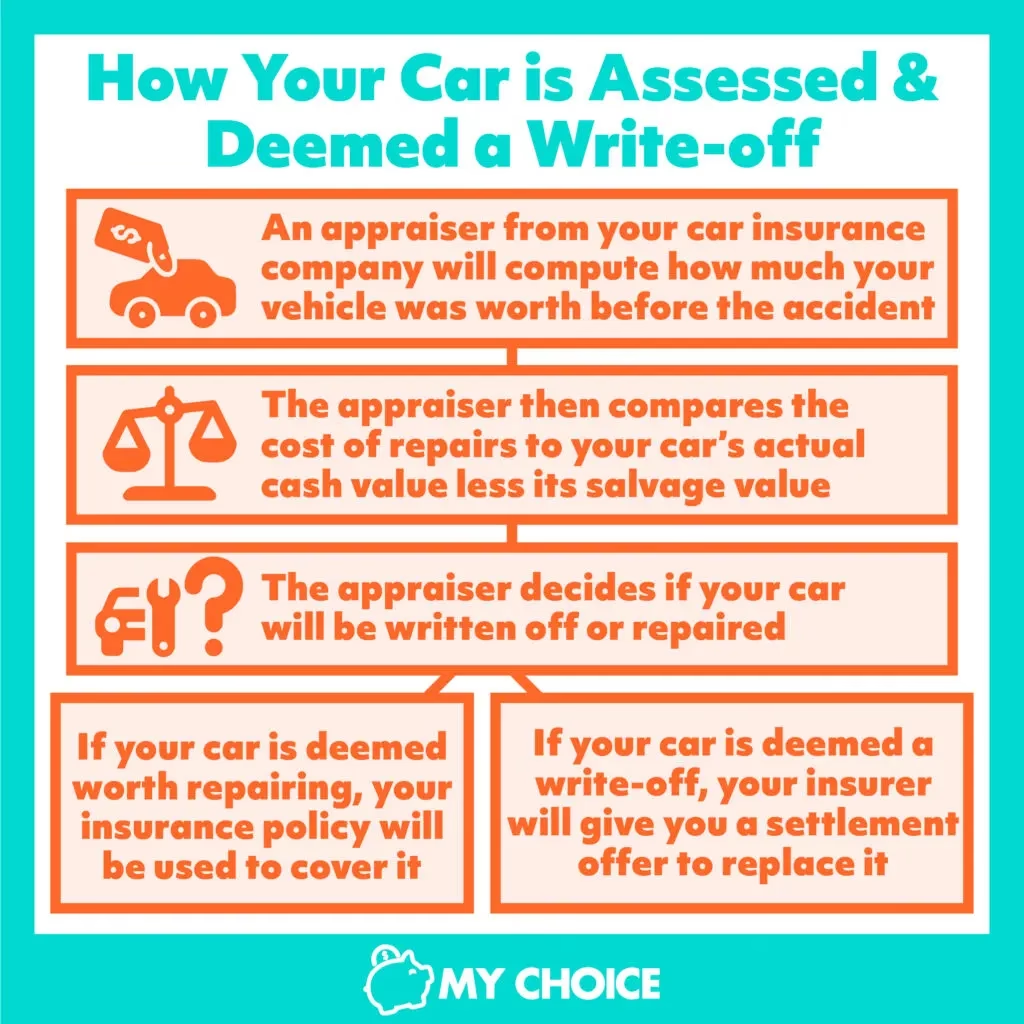

Scrapping a 'Write-Off' Vehicle

If your vehicle has been damaged to the extent that your insurance company deems it a 'write-off' (meaning it cannot be repaired economically), they will typically pay you the current market value of the vehicle rather than the cost of repairs. In this scenario, your insurer will usually handle the process of having your written-off vehicle sent to an Authorised Treatment Facility. It's beneficial to have a realistic idea of your vehicle's current market value beforehand, so you can be confident you're being offered a fair payout during the car insurance write-off procedure.

Replacing Your Scrapped Car with a New Vehicle

Many individuals will have a new car lined up to replace the one being scrapped. Naturally, most people want to avoid insuring two vehicles at once due to cost and administrative hassle. If you can time the delivery of your new car to coincide with the scrapping of your old one, you simply need to inform your insurer on the day. Provide them with the details of your new car, and they can amend your existing policy to cover your new vehicle.

If you're considering switching insurers, the change in vehicle is often an ideal opportunity. Some insurers may offer a partial refund if you've paid for the year upfront and have several months left on the policy. Others might hold you to the terms of your contract. In any case, it's always worth ringing your current insurer. Their customer service department's role is to keep you happy and retain your custom, so they may be willing to match quotes you've received from other providers.

Regarding when to insure your new car: you only need to insure it once it's on the road or parked on a public road. If the new vehicle is stored entirely on your private property and you're not yet driving it, there's no legal obligation to insure it. However, as noted previously, this means it won't be covered against damage or theft.

Essential Paperwork and Notifications

Properly managing your paperwork is paramount when scrapping a car to avoid legal and financial penalties.

- Authorised Treatment Facility (ATF): Always ensure your vehicle is scrapped through a legitimate ATF. They are licensed by the Environment Agency to depollute and dismantle end-of-life vehicles safely and legally.

- V5C Logbook: When the ATF collects your car, you must hand over your V5C logbook. However, it is absolutely crucial to retain the yellow section (Section 9 for older V5Cs or Section 4 for V5Cs issued after April 2019) which deals with selling, transferring, or part-exchanging a vehicle. The ATF will usually guide you through this to ensure you don't forget it.

- DVLA Notification: This is arguably the most important step. You must notify the DVLA that your vehicle has been scrapped. This is done by completing the retained section of your V5C and sending it to them. Delaying this notification can lead to a hefty fine of up to £1,000, as the DVLA will still consider you the registered keeper responsible for the vehicle.

- Certificate of Destruction (CoD): Once the ATF has processed your vehicle, they are legally required to issue you with a Certificate of Destruction. You should receive this within 7 days of the car being scrapped. This document is proof that your vehicle has been officially destroyed and removed from the DVLA's records. Keep this document safe for your records.

- Statutory Off Road Notification (SORN): If your vehicle was off the road and you had previously declared it SORN, this declaration will cease once the DVLA is notified of the scrapping. If you haven't declared it SORN and it's been off-road, it's a good idea to do so before collection, especially if you want a tax refund.

Frequently Asked Questions About Scrapping and Insurance

Here are answers to some common queries that arise when scrapping a car:

Is my vehicle insured during the scrapping process?

Your vehicle's insurance status during the scrapping process depends on its location. If it's on a public road, it must be insured until the scrap company collects it. Once collected, responsibility transfers to the scrap company, who will have their own insurance. If your car is on private property and you've declared it SORN, you are not legally required to have insurance, but it won't be covered for damage or theft during this period.

When does responsibility for the car pass from me to the scrap company?

Responsibility for the vehicle typically passes from you to the scrap company the moment they physically collect the vehicle from your premises. At this point, their insurance coverage for the vehicle takes effect.

Do I have to cancel my car insurance if I sell my car, or only when I scrap it?

Generally speaking, if you sell your car and it's no longer registered in your name, you are no longer legally required to maintain insurance on it. You cannot simply put the policy on hold for a future vehicle. Therefore, whether you sell or scrap your car, you should cancel the insurance policy to avoid paying for coverage you no longer need.

Will I be in trouble if I delay notifying my insurer of the scrapping?

While it's best practice to notify your insurer promptly, delaying this notification won't usually lead to legal trouble, but it will mean you continue to pay insurance premiums for a vehicle you no longer own or drive. The critical notification, which carries a significant penalty for delay, is to the DVLA. Failing to inform the DVLA that your car has been scrapped can result in a fine of up to £1,000.

Conclusion

Scrapping your car doesn't have to be a source of stress. By understanding the definition of a scrapped car, following the correct step-by-step process for disposal, and meticulously managing your insurance and paperwork, you can ensure a smooth transition. Remember the importance of using an Authorised Treatment Facility, notifying the DVLA promptly, obtaining your Certificate of Destruction, and communicating effectively with your insurer. Adhering to these guidelines will not only ensure compliance with UK regulations but also provide you with peace of mind, knowing your old vehicle has been handled responsibly.

If you want to read more articles similar to Scrapping Your Car: UK Insurance & Paperwork Guide, you can visit the Automotive category.