16/08/2023

When you've been involved in a car accident, the immediate aftermath can be a whirlwind of stress and uncertainty. While the usual course of action often involves contacting insurance companies or, in more severe cases, engaging legal professionals, there's another avenue that might be suitable for less complex situations: the car accident private settlement letter. This formal proposal, drafted by the injured party and sent to the breaching party, offers a pathway to resolve a road traffic incident outside the traditional, often protracted, legal system. It's an approach rooted in the desire for a swift, amicable, and cost-effective resolution, particularly when the injuries sustained are minor or the property damage is minimal.

This method allows both parties to avoid the significant time commitment, financial burden, and potential stress associated with formal lawsuits or extensive dealings with authorities. By opting for a private settlement, you're essentially seeking a direct agreement where the at-fault party compensates you for your financial losses and any physical harm incurred, without the need for court intervention. However, it's crucial to understand the nuances of this process, knowing when it's an appropriate choice and how to construct a letter that effectively communicates your intent and desired outcome.

- Why Consider a Private Settlement After a Car Accident?

- When is a Private Settlement Suitable?

- When to Avoid a Private Settlement

- Key Components of an Effective Private Settlement Letter

- Drafting Your Letter: A Step-by-Step Guide

- The Negotiation Process

- Understanding the Risks

- Frequently Asked Questions (FAQs)

- Conclusion

Why Consider a Private Settlement After a Car Accident?

The allure of a private settlement largely stems from its potential to streamline the resolution process. For many, the thought of navigating insurance claims, let alone court proceedings, is daunting. A private settlement offers several compelling advantages:

- Speed and Efficiency: Formal legal processes can drag on for months, even years. A private settlement can often be concluded much quicker, getting you compensated sooner.

- Cost-Effectiveness: Avoiding court means sidestepping hefty legal fees, court costs, and potentially even insurance premium increases. Both parties can save money.

- Privacy: Unlike court cases, which are public record, a private settlement keeps the details of your accident and its resolution confidential between the involved parties.

- Simplicity: For straightforward cases, a private settlement can be a far less bureaucratic and stressful experience than dealing with multiple insurance adjusters and legal teams. It offers an informal resolution.

- Flexibility: Parties have more control over the terms of the settlement, allowing for creative solutions that might not be possible within strict legal frameworks.

When is a Private Settlement Suitable?

While appealing, a private settlement isn't a one-size-fits-all solution. It's most appropriate for minor incidents where:

- Injuries are Minor or Non-Existent: If you've only suffered minor bumps, bruises, or no physical injuries at all, and your recovery is expected to be swift and without long-term complications.

- Property Damage is Minimal: When the damage to your vehicle or other property is superficial and quantifiable without extensive expert assessment. For instance, a scratched bumper or a broken wing mirror.

- Liability is Clear: Both parties agree on who was at fault for the accident, leaving little room for dispute.

- Both Parties are Willing to Cooperate: A successful private settlement hinges on the other party's readiness to negotiate and compensate you fairly.

- No Complex Issues: There are no other complicating factors like multiple vehicles involved, uninsured drivers, or pre-existing medical conditions that could be exacerbated.

When to Avoid a Private Settlement

Conversely, there are clear circumstances where pursuing a private settlement would be ill-advised and potentially detrimental:

- Serious Injuries: If you've sustained significant injuries, even if they don't seem severe immediately after the accident, their long-term impact and associated costs (medical treatment, lost earnings, pain and suffering) are often unpredictable and substantial. These cases require professional legal and medical evaluation.

- Significant Property Damage: When your vehicle is extensively damaged or a write-off, the costs can quickly escalate beyond what a private agreement can realistically cover or enforce.

- Disputed Liability: If there's any disagreement about who caused the accident, a private settlement is unlikely to succeed without formal investigation or legal intervention.

- Uninsured or Underinsured Drivers: If the other party doesn't have adequate insurance, enforcing a private settlement can become incredibly difficult if they refuse to pay.

- Emotional Distress or Psychological Harm: These damages are often hard to quantify and can have lasting effects, making them unsuitable for informal resolution.

- Lack of Trust: If you don't trust the other party to honour their agreement, a private settlement offers little recourse compared to a legally binding court order.

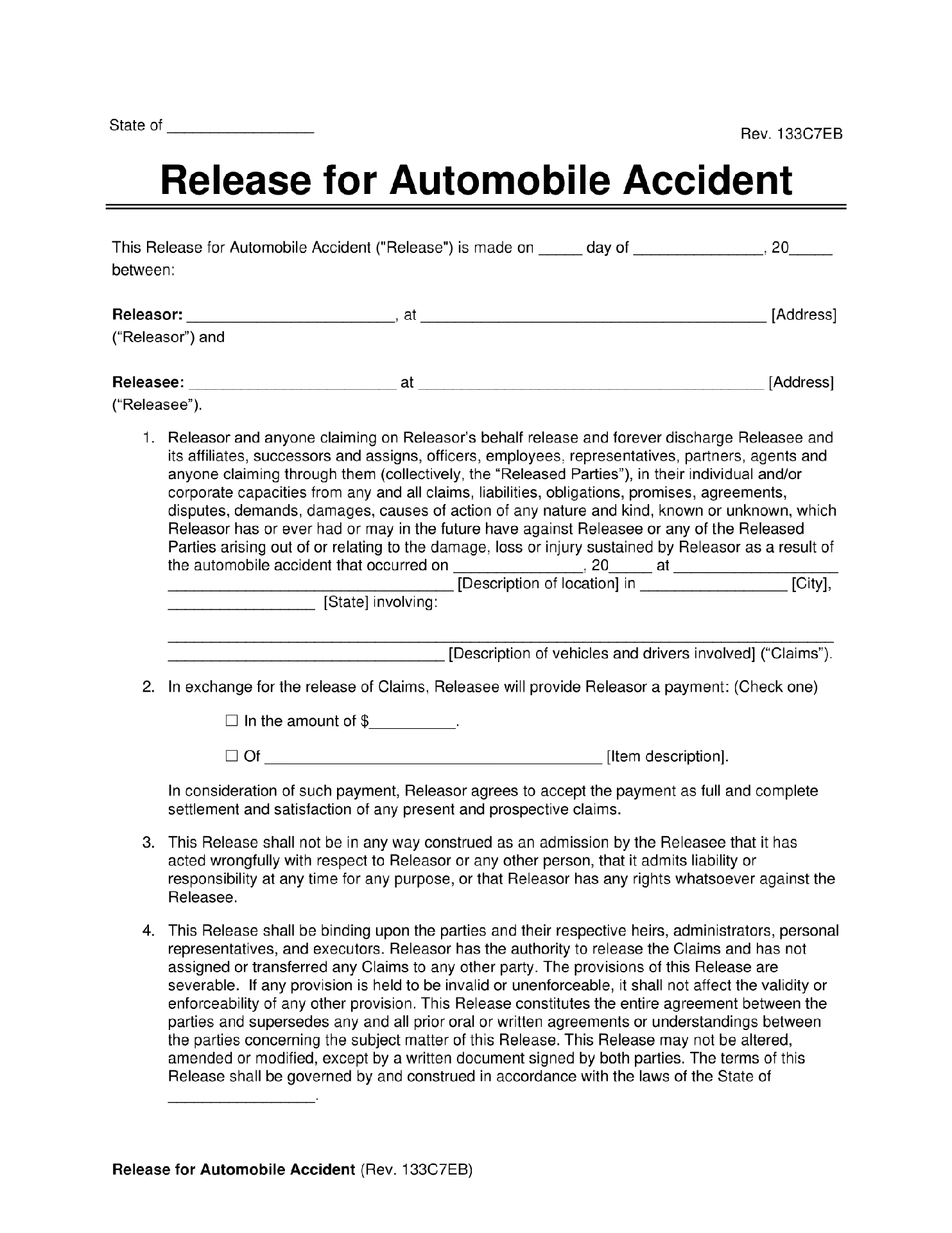

Key Components of an Effective Private Settlement Letter

To maximise your chances of a quick and positive response, your letter must be clear, professional, and comprehensive. Here are the essential elements to include:

- Your Contact Information and the Recipient's: Clearly state your full name, address, phone number, and email. Do the same for the recipient (the at-fault party).

- Date: The date the letter is sent.

- Reference: A clear subject line, e.g., 'Private Settlement Offer Regarding Car Accident on [Date]'.

- Salutation: Address the recipient politely by name.

- Introduction: Briefly introduce yourself and state the purpose of the letter – to offer a private settlement for the accident.

- Accident Details: Remind the recipient about the specific accident. Include the date, time, and exact location of the incident. Provide a brief, factual description of how the accident occurred, ensuring accuracy and avoiding emotional language.

- Summary of Damages/Injuries: Detail the specific damages to your vehicle (e.g., 'front bumper damage, broken headlight') and any physical injuries you sustained (e.g., 'whiplash, minor bruising to left arm'). Quantify these where possible, e.g., 'estimated repair cost £X', 'physiotherapy expenses £Y'. It's helpful to mention any evidence you have, such as photos of the damage or medical reports.

- Proposed Settlement Amount: Clearly state the exact monetary compensation you are seeking. This should be a precise figure.

- Justification for the Amount: Briefly explain how you arrived at this figure. Break down the costs:

| Category of Loss | Description | Amount (£) |

|---|---|---|

| Vehicle Repair | Quoted cost from garage for specific damages | [e.g., 850.00] |

| Medical Expenses | GP visits, prescriptions, physiotherapy | [e.g., 200.00] |

| Loss of Earnings | Days missed from work due to injury/recovery | [e.g., 150.00] |

| Miscellaneous Expenses | Travel for repairs, taxi fares while car was off road | [e.g., 50.00] |

| Pain and Suffering | Non-quantifiable discomfort (optional, for minor cases) | [e.g., 100.00] |

| Total Proposed Settlement | Sum of all categories | [e.g., 1350.00] |

- Payment Terms: Specify how and when you expect the payment (e.g., 'within 14 days of acceptance', 'via bank transfer').

- Release of Liability Clause: This is crucial. State that upon receipt of the full agreed-upon settlement amount, you will release the other party from any further claims related to this specific accident. This clause provides assurance to the paying party that this is a final settlement.

- Deadline for Response: Give a reasonable timeframe for them to respond (e.g., 7 or 14 days). This encourages a prompt reply and shows you are serious.

- Call to Action: Encourage them to contact you to discuss the matter further.

- Polite but Firm Tone: Maintain a professional and courteous tone throughout the letter. Avoid accusatory language or threats. While your goal is to make sure they understand the consequences of ignoring your offer (i.e., you may pursue other avenues like an insurance claim or legal action), this should be implied rather than explicitly stated as a threat.

- Closing: A professional closing, such as 'Sincerely' or 'Yours faithfully'.

- Your Signature: Sign the letter.

Drafting Your Letter: A Step-by-Step Guide

1. Gather All Documentation: Collect police reports (if any), photos of the scene and damages, repair estimates, medical bills, receipts for expenses, and any witness statements. The more evidence you have, the stronger your position.

2. Calculate Your Losses Accurately: Be realistic and precise. Overinflating your claim can deter the other party. Underestimating it means you might lose out. Use the table structure above as a guide.

3. Use Clear and Concise Language: Avoid jargon. The letter should be easy for anyone to understand.

4. Maintain a Professional Tone: Even if you're frustrated, a calm and rational letter is more likely to elicit a positive response. Remember, your goal is a mutual agreement.

5. Proofread Thoroughly: Errors can undermine your credibility. Check for spelling, grammar, and factual inaccuracies.

6. Send by Recorded Delivery: This provides proof that the letter was sent and received, which can be important if the matter escalates.

The Negotiation Process

Once your letter is sent, the other party might accept your offer, propose a counter-offer, or ignore it. If they counter-offer, be prepared to negotiate. This might involve adjusting your proposed amount slightly or agreeing on different payment terms. If an agreement is reached, it's essential to put it in writing, signed by both parties, detailing the agreed-upon amount, payment method, and the release of future liability. This written agreement serves as a private contract.

Understanding the Risks

While attractive, private settlements carry inherent risks:

- Enforcement Issues: If the other party agrees to pay but then defaults, enforcing the private agreement can be challenging without a formal legal framework. You might still end up in court to enforce the private contract.

- Undiscovered Damages/Injuries: What if a minor injury turns out to be more serious later? Or hidden damage to your car becomes apparent? A private settlement typically includes a release of future claims, meaning you can't go back and ask for more money later. This is why seeking legal advice is crucial, especially concerning future claims.

- Inadequate Compensation: Without expert assessment from insurance adjusters or legal professionals, you might undervalue your claim.

- Lack of Formal Record: While privacy is a benefit, the lack of a formal, public record can be a disadvantage if future disputes arise.

Frequently Asked Questions (FAQs)

Q: Do I need a solicitor to write a private settlement letter?

A: For minor incidents, you can draft it yourself. However, for anything beyond very trivial matters, consulting a solicitor is highly recommended to ensure your rights are protected and the letter is legally sound.

Q: What if the other party ignores my letter?

A: If your letter is ignored, you may need to escalate the matter. This could involve contacting your own insurance company to file a claim, or, if appropriate, pursuing a small claims court action.

Q: Can I include 'pain and suffering' in a private settlement?

A: Yes, you can include a reasonable amount for pain and suffering, especially if it resulted in inconvenience or minor discomfort. However, quantifying this can be subjective, and it's easier to justify with medical evidence for more significant injuries.

Q: Should I involve my insurance company at all?

A: It's often advisable to at least inform your insurance company of the accident, even if you intend to settle privately. Your policy may require you to report all accidents. They might also offer advice or assistance, even if not directly handling the claim initially. Be aware that most policies have specific reporting timelines.

Q: What if I discover more damage or injury after settling?

A: This is a significant risk. Most private settlement agreements include a clause releasing the at-fault party from future claims. If you sign such an agreement, you generally cannot seek further compensation later, even if new issues arise. This underscores the importance of being certain about the full extent of damages before settling.

Conclusion

A car accident private settlement letter can be an effective tool for resolving minor road traffic incidents efficiently and privately. It offers a pathway to avoid the complexities and costs associated with formal legal proceedings, leading to a quicker resolution and potentially less stress for all involved. However, it is not a suitable option for every situation. Before embarking on this path, thoroughly assess the extent of damages and injuries, confirm liability, and ensure the other party is willing to cooperate. Careful drafting of the letter, clear communication, and a realistic expectation of outcomes are paramount. For any situation beyond the most trivial fender-bender, seeking professional legal advice is always the safest course of action to ensure your rights are protected and you receive fair compensation for your losses.

If you want to read more articles similar to Private Settlement Letters for Car Accidents, you can visit the Automotive category.