01/12/2016

Receiving a penalty notice from the Driver and Vehicle Licensing Agency (DVLA) can be an unsettling experience. Whether it's for an untaxed vehicle, a lapse in your MOT, or failing to declare a Statutory Off Road Notification (SORN), these notices demand your immediate attention. While it might be tempting to tuck them away and hope they disappear, ignoring a DVLA penalty is a decision that can lead to far more severe consequences than the initial fine. This article delves into the escalating chain of events that unfolds when a DVLA penalty goes unpaid, outlining the financial, legal, and personal repercussions you could face.

- Understanding DVLA Penalties

- The Escalation Ladder: What Happens When You Don't Pay?

- Stage 1: The Initial Penalty Notice

- Stage 2: Increased Fines and Reminder Letters

- Stage 3: Referral to a Debt Collection Agency

- Stage 4: County Court Judgment (CCJ)

- Stage 5: Enforcement Agents (Bailiffs)

- Stage 6: Vehicle Clamping and Impounding

- Stage 7: Potential Prosecution and Driving Licence Implications

- Wider Consequences Beyond the Fine

- Comparative Costs: Paying vs. Ignoring

- What To Do If You Receive a DVLA Penalty

- Preventative Measures

- Frequently Asked Questions (FAQs)

- Q: Can I go to prison for not paying a DVLA penalty?

- Q: How long does a CCJ stay on my credit file?

- Q: What if I sold the vehicle? Am I still liable?

- Q: Can I appeal a DVLA penalty after the deadline?

- Q: Is there a statute of limitations for DVLA penalties?

- Q: What's the difference between a DVLA fine and a parking ticket?

Understanding DVLA Penalties

The DVLA is responsible for maintaining a register of drivers and vehicles in Great Britain. Their penalties are designed to ensure compliance with motoring laws, promoting road safety and fair taxation. Common DVLA-related penalties include:

- Failure to tax a vehicle: Driving or keeping an untaxed vehicle on a public road.

- No valid MOT: Driving a vehicle without a current MOT certificate.

- Failure to declare SORN: Keeping a vehicle off-road but failing to declare it as SORN.

- Not notifying DVLA of a change of ownership: Failing to inform the DVLA when you buy or sell a vehicle.

- Driving without a valid driving licence: Though often a police matter, the DVLA is integral to licensing.

It's crucial to understand that these aren't just minor administrative oversights. Each penalty carries a specific fine, and the process for non-payment is robust and designed to ensure compliance.

The Escalation Ladder: What Happens When You Don't Pay?

Ignoring a DVLA penalty doesn't make it go away; it merely triggers a series of escalating actions, each with more severe implications. Here's a breakdown of what you can expect:

Stage 1: The Initial Penalty Notice

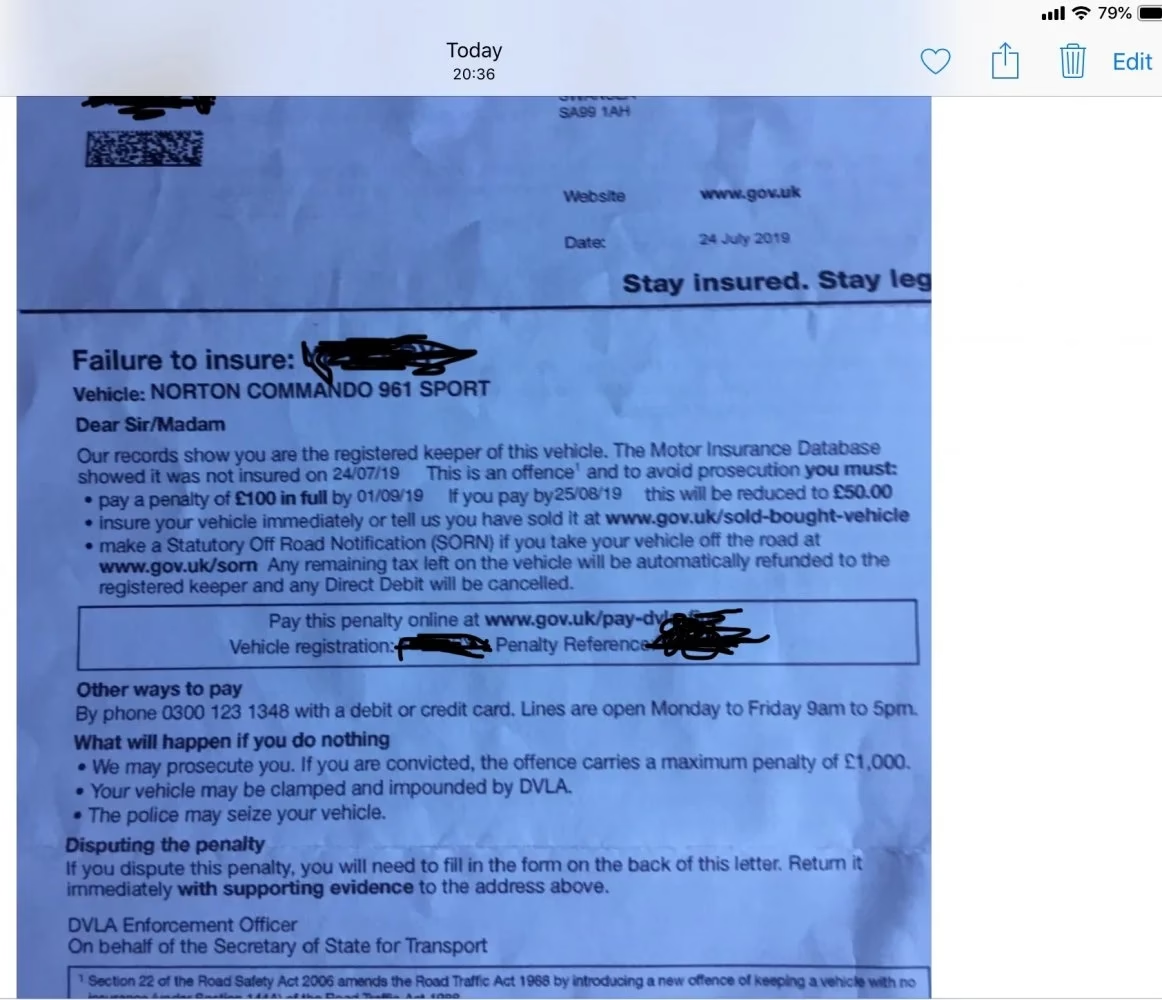

Upon detection of an offence, the DVLA will issue an initial Fixed Penalty Notice (FPN). This notice will detail the offence, the amount of the fine (e.g., £80 or £100 for many untaxed or SORN offences), and the deadline for payment, usually 28 days. It will also outline how to pay or how to appeal if you believe the penalty was issued in error. At this stage, paying the fine promptly is the simplest and cheapest resolution.

Stage 2: Increased Fines and Reminder Letters

If the initial penalty is not paid by the deadline, the DVLA will typically issue reminder letters. These letters often include an increased fine amount. For example, an £80 penalty might double to £160. This increase is designed to encourage immediate payment and cover the administrative costs of pursuing the outstanding debt. Ignoring these reminders is a critical mistake, as it signals to the authorities that further action is required.

Stage 3: Referral to a Debt Collection Agency

Should the increased fine remain unpaid, the DVLA will likely pass the debt to a third-party debt collection agency. These agencies are authorised to pursue the outstanding amount on behalf of the DVLA. They will send their own letters, make phone calls, and may even send representatives to your home. Crucially, their involvement adds further fees to your original debt. These administrative and collection charges can significantly inflate the amount you owe, sometimes by hundreds of pounds. While they cannot seize goods without a court order at this stage, their presence adds considerable pressure and stress.

Stage 4: County Court Judgment (CCJ)

If the debt collection agency is unsuccessful, the DVLA (or the agency acting on their behalf) may apply to the County Court for a County Court Judgment (CCJ) against you. A CCJ is a court order that formally confirms you owe money to the DVLA. If a CCJ is issued against you and you fail to pay it within one month, it will be registered on your credit score for six years. This has severe implications for your financial future, making it extremely difficult to obtain loans, mortgages, credit cards, or even some mobile phone contracts. It essentially signals to lenders that you are a high-risk borrower.

Stage 5: Enforcement Agents (Bailiffs)

Once a CCJ is granted, and if the debt remains unpaid, the DVLA can apply for a warrant of control. This allows enforcement agents, commonly known as bailiffs, to visit your property to seize goods to the value of the debt, plus their own substantial fees. Bailiffs have legal powers to enter your home (though usually not by force on the first visit for unpaid fines) and take items like vehicles, electronics, or other valuables. The fees charged by bailiffs are regulated but can be very high, potentially adding hundreds of pounds to the original debt, making an already difficult situation much worse.

Stage 6: Vehicle Clamping and Impounding

For offences directly related to vehicle compliance (e.g., untaxed or uninsured vehicles), the DVLA or their enforcement partners have powers to clamp your vehicle or even impound it immediately. If your vehicle is clamped, you'll need to pay a release fee and the outstanding tax/fine to get it released. If it's impounded, you'll face daily storage charges on top of the release fee and any outstanding debts. If you don't collect your vehicle within a specified period, it can be crushed. This is a very direct and impactful consequence, as it removes your mode of transport.

Stage 7: Potential Prosecution and Driving Licence Implications

For more serious or persistent offences, or if you fail to comply with court orders, the DVLA can pursue prosecution in a magistrates' court. This can result in much higher fines (potentially up to £1,000 or even £2,500 for some offences), penalty points on your driving licence, or even disqualification from driving. While rare for simple non-payment of a fixed penalty, repeatedly ignoring warnings and court orders can escalate to criminal proceedings. In extreme cases, and for very serious offences or contempt of court, imprisonment is a theoretical possibility, though highly unlikely for a standard unpaid fine.

Wider Consequences Beyond the Fine

The impact of an unpaid DVLA penalty extends beyond just the escalating financial costs:

- Damage to Your Credit Rating: As mentioned, a CCJ will severely impact your ability to secure credit for six years.

- Stress and Anxiety: Dealing with debt collectors and bailiffs is incredibly stressful and can significantly affect your mental well-being.

- Loss of Assets: The threat or reality of bailiffs seizing your possessions is a frightening prospect.

- Legal Complications: Court appearances and legal proceedings are time-consuming and daunting.

- Loss of Vehicle: For offences like untaxed vehicles, you risk losing your car entirely.

Comparative Costs: Paying vs. Ignoring

To illustrate the financial folly of ignoring a DVLA penalty, consider this simplified comparison:

| Action Stage | Example Cost (Untaxed Vehicle) | Notes |

|---|---|---|

| Initial Fixed Penalty (Paid Promptly) | £80 - £100 | Simplest and cheapest resolution. |

| After Reminder/Increased Fine | £160 - £200 | Fine has doubled. |

| After Debt Collection Agency Involvement | £250 - £400+ | Original fine + agency fees. |

| After County Court Judgment (CCJ) | £300 - £600+ | Original fine + agency fees + court costs. Damages credit score. |

| After Bailiff Action | £600 - £1,000+ | Original fine + agency fees + court costs + substantial bailiff fees. Risk of goods seizure. |

| Vehicle Clamping/Impounding | £100+ Release Fee + Daily Storage + Outstanding Tax/Fine | Direct vehicle seizure. Can lead to vehicle crushing. |

As you can see, the cost of ignoring a penalty quickly escalates, making the initial fine seem negligible in comparison.

What To Do If You Receive a DVLA Penalty

If you find yourself in receipt of a DVLA penalty notice, here's the best course of action:

- Do Not Ignore It: This is the most crucial piece of advice. Burying your head in the sand will only make matters worse.

- Read Carefully: Understand why the penalty was issued, the amount, and the deadline for payment or appeal.

- Verify the Details: Check that the vehicle details, date, and alleged offence are correct.

- Pay if Applicable: If the penalty is valid and you accept it, pay it promptly by the deadline. This will save you significant money and stress in the long run.

- Appeal if Incorrect: If you genuinely believe the penalty was issued in error (e.g., you had already declared SORN, or sold the vehicle), follow the instructions on the notice to appeal. Gather any evidence you have to support your case.

- Seek Advice if Struggling: If you are genuinely unable to pay the fine, it's advisable to seek independent debt advice from organisations like Citizens Advice or National Debtline. While the DVLA might not offer payment plans, these organisations can help you understand your options when dealing with debt collectors or court orders.

Preventative Measures

Avoiding DVLA penalties in the first place is always the best strategy:

- Keep Your Vehicle Taxed: Set up a direct debit for vehicle tax, or set reminders for annual renewal.

- Ensure Your MOT is Current: Always get your MOT done before it expires.

- Declare SORN Correctly: If your vehicle is off-road and not taxed, ensure you have a valid SORN in place.

- Update Your Details: Inform the DVLA immediately of any change of address or name.

- Notify of Change of Ownership: When buying or selling a vehicle, ensure the V5C (logbook) is correctly updated with the DVLA. This protects you from future penalties related to the vehicle.

Frequently Asked Questions (FAQs)

Q: Can I go to prison for not paying a DVLA penalty?

A: It's highly unlikely for a standard unpaid DVLA fixed penalty. However, if the matter goes to court and you repeatedly fail to comply with court orders (e.g., payment plans), or if the original offence was very serious (e.g., driving whilst disqualified), then contempt of court or the underlying serious offence could carry a prison sentence. For most unpaid fines, the consequences are financial and credit-related.

Q: How long does a CCJ stay on my credit file?

A: A County Court Judgment (CCJ) remains on your credit file for six years from the date it was issued, regardless of whether you pay it off. If you pay the CCJ in full within one month of it being issued, it will be removed from your file. After one month, if paid, it will be marked as 'satisfied' but will still remain on your file for the full six years.

Q: What if I sold the vehicle? Am I still liable?

A: If you sold the vehicle and properly notified the DVLA of the change of ownership using the V5C logbook, then you should not be liable for penalties incurred by the new owner. However, if you failed to notify the DVLA, you might still be held responsible for offences related to that vehicle. Always keep proof of postage or an acknowledgment from the DVLA when notifying them of a sale.

Q: Can I appeal a DVLA penalty after the deadline?

A: It becomes significantly harder to appeal after the initial deadline. You might have limited options if the case has progressed to court. It's always best to appeal within the specified timeframe if you believe the penalty is incorrect.

Q: Is there a statute of limitations for DVLA penalties?

A: For fixed penalty notices, the DVLA typically has six months from the date of the offence to start court proceedings. However, once a court order like a CCJ is obtained, the debt can be enforced for a much longer period, and the DVLA (or their agents) can pursue it for many years.

Q: What's the difference between a DVLA fine and a parking ticket?

A: A DVLA fine is issued by the Driver and Vehicle Licensing Agency for offences related to vehicle tax, MOT, SORN, and registration. A parking ticket (Penalty Charge Notice or PCN) is usually issued by a local council or private parking company for parking infringements. While both are financial penalties, they come from different authorities and have different enforcement processes.

In conclusion, ignoring a DVLA penalty is a perilous path. What starts as a relatively small fine can quickly balloon into a significant financial burden, damage your credit rating, and even lead to the loss of your vehicle or severe legal repercussions. The best course of action is always to address the penalty promptly, either by paying it or by lodging a legitimate appeal. Staying compliant with motoring regulations not only keeps you on the right side of the law but also protects your financial well-being and peace of mind.

If you want to read more articles similar to Unpaid DVLA Penalties: What Happens Next?, you can visit the Motoring category.