19/12/2023

The automotive industry is in the midst of a profound transformation, driven largely by the advent of connected cars. These intelligent vehicles are far more than just modes of transport; they are sophisticated data hubs, continuously generating streams of valuable information. For mobility companies, including original equipment manufacturers (OEMs), suppliers, dealers, insurers, and fleet operators, this data represents an unparalleled opportunity to redefine business models, enhance customer experiences, and unlock significant financial benefits. While the full potential of this data is still being realised, the shift from a hardware-centric approach to one focused on software-as-a-service (SaaS) and subscription-based offerings is rapidly gaining momentum, promising a future where data is as valuable as the vehicle itself.

- What Exactly is Connected Car Data?

- The Unveiled Potential: Why Connected Cars Matter for Mobility Companies

- Monetising the Data: A Multi-Billion Pound Opportunity

- Overcoming Hurdles: The Slow March to Data Monetisation

- Five Imperatives for Success in Connected Car Data

- 1. Ensuring Short-Term Profitability and Solid Long-Term Investments

- 2. Improving the Customer Experience

- 3. Using Data to Respond to Regulatory Pressures and New Security Requirements

- 4. Taking Advantage of New Opportunities

- 5. Increasing the Importance of Life-Cycle Monetisation and New Business Models

- Key Use Cases: Driving Value Across the Lifecycle

- Building the Future: Essential Capabilities for Data Monetisation

- Frequently Asked Questions About Connected Cars and Mobility

- Q1: How much value can connected cars realistically add to the mobility industry?

- Q2: What are the biggest challenges mobility companies face in monetising connected car data?

- Q3: How do regulations like GDPR affect connected car data monetisation?

- Q4: What are the most impactful use cases for connected car data?

- Act Now to Successfully Participate in Car-Data Monetisation

What Exactly is Connected Car Data?

At its core, connected car data refers to the vast array of information collected and transmitted by vehicles equipped with internet connectivity. This data is gathered through various onboard systems, primarily the vehicle's Electronic Control Units (ECUs) and Controller Access Networks (CANs). These systems monitor virtually every aspect of a vehicle's operation, from its mechanical performance to the driver's interactions with its features.

The collected data is then transmitted wirelessly, typically over mobile data networks using integrated SIM cards, to central servers via telematics systems connected through the cloud. This allows for remote, real-time monitoring and analysis of numerous vehicle attributes. Examples of the rich data points collected include:

- Vehicle location and journey history

- Speed and acceleration patterns

- Fuel consumption and battery status

- Engine performance and fault codes

- Tyre pressures and braking habits

- Locking status and security alerts

- Usage patterns of in-car features and infotainment systems

A single connected vehicle can generate up to 30 terabytes of data per day, though only a portion of this is typically transmitted over the air to central operations. This wealth of information forms the foundation for a multitude of applications, many of which are still emerging, ranging from sophisticated fleet management and predictive maintenance to urban planning and personalised insurance offerings.

The Unveiled Potential: Why Connected Cars Matter for Mobility Companies

Connected cars offer a unique blend of benefits, simultaneously delivering enhanced customer experiences and substantial cost and revenue advantages for mobility companies. The ability to collect and analyse real-time vehicle data allows for unprecedented insights into vehicle performance, driver behaviour, and market trends.

Enhancing Customer Experience and Loyalty

Consumers increasingly value connectivity. Surveys indicate that a significant percentage of respondents, globally and even more so in certain markets like China, would switch car brands for improved connectivity features. Furthermore, a substantial portion of consumers are interested in unlocking additional digital features after purchasing a vehicle. This highlights a clear demand for advanced, flexible, and evolving in-car experiences. OEMs that fail to meet this rising expectation risk losing customers to competitors who prioritise digital innovation.

Connected services enable a continuous engagement model with the customer, moving beyond the one-off sale. Features like remote vehicle monitoring, personalised infotainment, and real-time navigation updates can significantly improve driver satisfaction and foster brand loyalty. The ability to deliver Over-the-Air (OTA) updates, akin to smartphone software updates, ensures that a vehicle's capabilities can evolve and improve throughout its life-cycle, keeping it fresh and relevant for longer.

Driving Cost Efficiencies and New Revenue Streams

The monetisation of connected car data extends far beyond just selling subscription services to end-users. It encompasses a broad spectrum of opportunities to generate value:

- Tailored Insurance: Insurers can leverage driving style data to offer usage-based insurance, rewarding safer drivers with lower premiums.

- Predictive Maintenance: By analysing component usage and status data, vehicles can predict potential failures, allowing for proactive maintenance that reduces costly breakdowns and increases vehicle uptime for fleet operators. This also drives repair traffic to OEM-approved channels.

- R&D Optimisation: Real-time data from vehicle fleets can inform future vehicle design and specifications, allowing OEMs to deprioritise unused features or adjust component specifications, potentially saving billions in development costs.

- Targeted Advertising: Media agencies can increase their advertising reach through new touch points inside and outside of vehicles, leveraging contextual data.

- Smart City Solutions: Cities can use sensory data to identify potholes, optimise traffic flow, and monitor pollution levels, improving urban infrastructure and quality of life.

- New Business Models: The shift towards subscription services for premium connectivity, advanced driver-assistance systems (ADAS), and even performance upgrades creates recurring revenue streams.

These benefits are not just theoretical; they are already being realised by pioneering companies. However, many in the automotive sector have been slow to fully capitalise on these opportunities, leading to a slower uptake in data monetisation than initially anticipated.

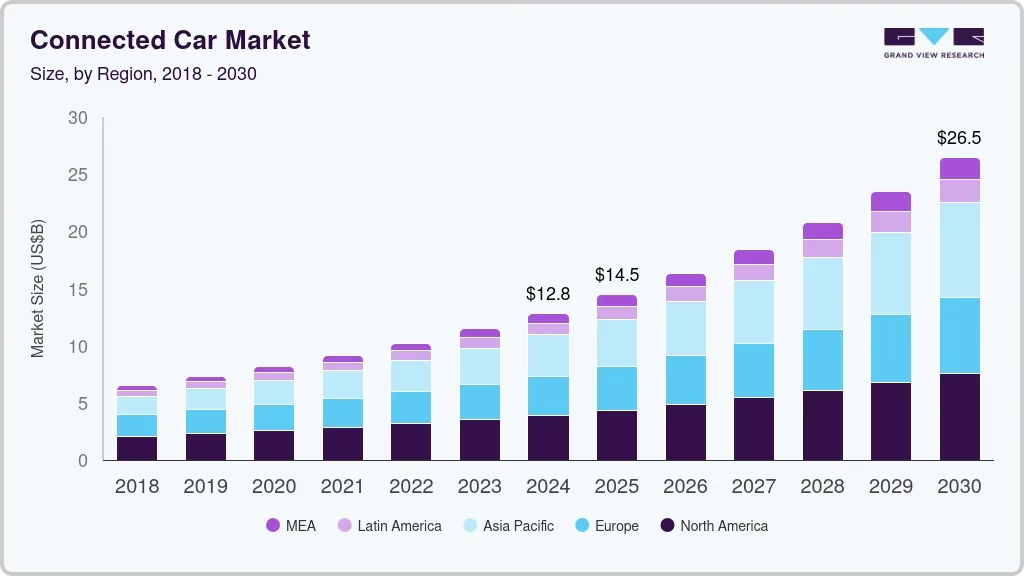

Monetising the Data: A Multi-Billion Pound Opportunity

The potential market value of data-based services from connected cars is immense. Forecasts suggest that these services could deliver between $250 billion and $400 billion in annual incremental value for players across the ecosystem by 2030. This includes both additional revenue generated from services and data sales, as well as significant cost savings enabled by car data.

On a per-vehicle level, this translates to an average of up to $310 in revenue and $180 in cost savings per year by 2030. The value varies significantly based on the level of connectivity:

| Connectivity Level (C3X Framework) | Revenue Potential (USD) | Cost Savings (USD) |

|---|---|---|

| Basic (Levels 1-2) | $130 - $210 | $100 - $170 |

| Advanced (Levels 4-5) | $400 - $610 | $120 - $210 |

The Connected Car Customer Experience (C3X) Framework

To better understand the evolution of connectivity, McKinsey's C3X framework outlines five levels of user experience:

- Level 1 (Basic Connectivity): Focuses on general hardware connectivity, allowing drivers to track basic vehicle usage and monitor technical status.

- Level 2 (Basic Connectivity): The vehicle can use a driver's personal profile to access digital services via external digital ecosystems.

- Level 3 (Intermediate Connectivity): The focus shifts to all occupants, who enjoy personalised controls, infotainment, and advertising.

- Level 4 (Advanced Connectivity): Occupants engage in live multimodal dialogues with the vehicle in real-time and receive proactive recommendations.

- Level 5 (Advanced Connectivity): The vehicle acts as a virtual chauffeur, using cognitive artificial intelligence to meet explicit and unstated needs of occupants.

By 2030, nearly 95% of new vehicles sold globally are expected to be connected, a significant jump from around 50% today. Crucially, about 45% of these will feature intermediate and advanced connectivity, dramatically expanding the addressable market for sophisticated solutions.

Overcoming Hurdles: The Slow March to Data Monetisation

Despite the evident potential, many companies, particularly traditional OEMs, have struggled to fully capitalise on connected car data. Several factors explain this slower-than-anticipated progress:

- Failing to Generate Customer Interest: Consumers are accustomed to 'free' connectivity services on smartphones. OEMs face the challenge of convincing them that car-connectivity services offer additional, differentiated value, especially given often complex onboarding processes.

- Organisational Inertia: Many companies have not adequately reshaped their organisations to build the necessary capabilities for effective data monetisation across the entire vehicle life-cycle. Siloed functions, talent acquisition challenges, and an outdated focus on point-of-sale revenues rather than recurring, life-cycle value hinder progress.

- Lack of Ecosystem Development: Automakers often work in isolation, developing 'island solutions' rather than collaborating with existing infrastructure, service, and data providers. Scaling these solutions quickly and delivering sought-after benefits requires robust ecosystems and partnerships.

- Technical Challenges: The development of robust Electrical/Electronic (E/E) architectures capable of handling massive data flows and enabling seamless OTA updates has taken longer than expected.

- Economic Pressures: A tightening economic situation and the impact of global events like COVID-19 have reduced investments in connectivity, further slowing progress.

Five Imperatives for Success in Connected Car Data

To accelerate progress and fully realise the value of connected car data, mobility companies must focus on five critical imperatives:

1. Ensuring Short-Term Profitability and Solid Long-Term Investments

Companies face a dual transformation: making core businesses profitable amidst headwinds (e.g., ICE bans, regulations) while simultaneously investing heavily in new E/E architectures, software, EVs, and autonomous vehicle (AV) technology. Connected services offer a near-term revenue and profit opportunity due to relatively low initial investments, faster development timelines, high margins, and recurring revenue streams.

2. Improving the Customer Experience

OEMs have direct customer access, a powerful asset for monetisation. However, poor customer experience, complex sign-up processes, and challenging interfaces often lead to low retention rates. New EV OEMs are setting higher standards by leveraging customer feedback, rapid iteration, and OTA updates. Traditional players must emulate this customer-centric approach, competing not just with peers but with the best high-tech players to provide seamless, intuitive digital interactions.

3. Using Data to Respond to Regulatory Pressures and New Security Requirements

Increasingly strict data regulations (e.g., GDPR, CCPA) provide a clearer framework for data use, rather than limiting it. Thorough guidance, especially in the EU, offers legal security for handling personal information, potentially encouraging more personalised data sales. Beyond regulation, cybersecurity is paramount for connected vehicles. Industry initiatives, such as those from WP.29, mandate robust cybersecurity throughout the development process and via OTA updates. These pressures can prompt OEMs to re-examine their data approaches, making information more widely available within their ecosystems and unlocking new monetisation opportunities through increased information sharing.

4. Taking Advantage of New Opportunities

The forecast dramatic increase in connectivity levels (60-70% of new vehicles in North America and Europe reaching C3X Level 3 or above by 2030) will significantly expand the market. More powerful E/E architectures, improved sensors (cameras, LiDAR), and increased computing power are enabling a wider range of services. New EV OEMs are leading the way in popularising OTA updates and advanced E/E architectures, effectively setting new industry standards. OEMs must strategically define their 'make-versus-buy' strategies, identifying key differentiating control points to compete effectively, or risk becoming mere vehicle assemblers as tech players integrate their ecosystems into vehicles.

5. Increasing the Importance of Life-Cycle Monetisation and New Business Models

The automotive industry is shifting away from a sole focus on point-of-sale revenues. Online vehicle sales and subscription models are gaining popularity, reinforcing the importance of a life-cycle perspective. OEMs and suppliers are exploring OTA feature updates and connected-service unlocks to generate new revenue streams throughout a vehicle's life. Examples include selling acceleration updates, offering connectivity packages by subscription, or providing innovative services like mobile charging or 'office mode' features. These recurring interactions build customer loyalty and open up diverse profit avenues, whether through direct consumer sales, data marketplaces, or partnerships with insurers and mobility providers.

Key Use Cases: Driving Value Across the Lifecycle

Connected car data enables a multitude of use cases that deliver value throughout the vehicle life cycle. Three stand out for their significant impact:

Over-the-Air (OTA) Updates, Upgrades, and Unlocks

OTA capabilities are transformative. They allow OEMs and suppliers to sell new software-based features to vehicles already in the fleet, post-production. This includes adding new features to infotainment systems, activating hardware functionalities, and resolving software issues remotely. Beyond generating revenue from end-users, OTA updates can reduce residual value losses for dealers by adding missing features and significantly cut costs by preventing or accelerating recalls. They also allow for reduced manufacturing complexity by enabling a 'single hardware, multiple features' approach.

For OTA to be successful, OEMs need robust, modular E/E architectures and software with sufficient spare capacity. The business case must extend beyond the initial sale, with feature road maps planned well into the vehicle's life. This also opens new cooperation and revenue-sharing models with suppliers.

R&D Hardware Optimisation

Leveraging real-time data from the vehicle fleet allows OEMs and suppliers to adjust vehicle specifications and features based on actual usage patterns. Unlike traditional methods relying solely on historical data, this approach enables more informed decisions. For instance, if real-time data shows a feature is barely used, it can be deprioritised in future models, or component specifications can be refined based on wear and tear data. This can lead to billions in savings by streamlining variant management and rectifying issues across new vehicles and existing fleets much faster.

Predictive Maintenance

This use case relies on data about component usage and status to anticipate and prevent costly vehicle failures. For OEMs and dealers, it increases repair traffic within their own channels. Fleet operators benefit from increased uptime by avoiding unscheduled repairs and breakdowns. Insurers can save significant sums by preventing accidents linked to component wear. Furthermore, vehicles could proactively schedule repairs, optimise inventory for service departments, and even adjust settings to reduce wear and tear, lowering overall maintenance costs.

Building the Future: Essential Capabilities for Data Monetisation

To capture the immense value offered by connected car data, players across the mobility ecosystem need to develop four core capabilities:

1. Double Down on a Customer-Centric Approach

Monetisation must be driven by what customers want and are willing to pay for. This involves conducting customer clinics to map out pain points and identify desired features. The development process must be continuous, extending beyond the initial sale, with ongoing user testing and frequent software updates to ensure high engagement. Companies need dedicated customer satisfaction teams to collect usage data and inform future releases, ensuring features are actively used and perceived value is high. This approach, common in leading SaaS companies, is crucial for improving retention in subscription models.

2. Get Technical Enablers Right

The vehicle's E/E architecture, software, and operating system (OS) must be designed for upgradability and maintainability, with hardware-abstraction layers and sufficient performance reserves. Back-end systems must support regular OTA updates efficiently. Companies need a robust 'make-versus-buy' strategy, identifying key control points where they must develop in-house capabilities versus integrating external systems (e.g., voice assistants). No single company will possess all necessary capabilities, necessitating strategic partnerships.

3. Choose an Operating Model for a Digital Business

Successful data monetisation requires dedicated, cross-functional teams spanning R&D, marketing, sales, legal, and finance. These teams, rare in traditional automotive but common in tech and SaaS, enable rapid development and deployment of use cases across the entire vehicle life-cycle. They foster agile work processes, flat hierarchies, and rapid iteration from idea generation to implementation, significantly boosting productivity and reducing launch delays. Hiring the right talent, particularly software developers, is paramount.

4. Fully Leverage a Digital Go-to-Market (GTM)

Players must develop sophisticated digital GTM skills. While some, like insurance companies, already excel in digital channels, OEMs need to catch up. This means moving beyond fragmented, country-specific approaches to a coordinated multichannel strategy that leverages mobile apps, websites, social media, and dealer networks. The focus must shift from one-off hardware sales to continuous customer interaction through context-driven performance marketing, often involving partners within the expanding automotive ecosystems.

Frequently Asked Questions About Connected Cars and Mobility

Q1: How much value can connected cars realistically add to the mobility industry?

Forecasts indicate connected cars could add between $250 billion and $400 billion in annual incremental value by 2030, through a combination of new revenue streams from services and data sales, alongside significant cost savings across the value chain. On a per-vehicle basis, this could average up to $310 in revenue and $180 in cost savings annually.

Q2: What are the biggest challenges mobility companies face in monetising connected car data?

Key challenges include generating sufficient customer interest and differentiating services from smartphone offerings, organisational inertia (siloed departments, talent gaps, outdated business cases), and a failure to establish robust ecosystems and partnerships. Technical complexities in E/E architectures and economic pressures also play a role.

Q3: How do regulations like GDPR affect connected car data monetisation?

Rather than hindering progress, strong data regulations like GDPR provide a clear legal framework for handling personal data, offering greater legal security for companies. This can actually encourage more widespread and responsible data sharing within ecosystems, potentially unlocking new monetisation opportunities by defining clear boundaries and responsibilities.

Q4: What are the most impactful use cases for connected car data?

Three use cases are expected to deliver the greatest impact, accounting for 40-45% of the total value pool: Over-the-Air (OTA) updates, upgrades, and unlocks; R&D hardware optimisation; and predictive maintenance. These leverage data to generate recurring revenues, reduce development costs, and improve vehicle reliability and uptime.

Act Now to Successfully Participate in Car-Data Monetisation

The automotive industry's connectivity landscape is evolving at an unprecedented pace, significantly increasing the potential for data monetisation across the entire ecosystem. Data suppliers, such as OEMs and vehicle fleets, are uniquely positioned to benefit, as are insurance providers, aftermarket companies, city planners, and infrastructure operators. Given the current underperformance in data monetisation, innovative new players could rapidly gain a competitive edge over slower-moving incumbents. Those who hesitate risk missing out on a critical opportunity to differentiate themselves in one of the industry's most vital customer-facing spaces. While awareness of this imperative is growing, consistent development of compelling new offers and services remains a challenge. Failure to adapt to rising customer expectations and rapid technological advancements could erode brand appeal and profit pools, leading to market share decline. Conversely, those who proactively harness this opportunity will unlock new profit pools and enable sustained, profitable growth for the industry.

If you want to read more articles similar to Connected Cars: Powering Mobility's Future, you can visit the Automotive category.