20/11/2006

PCP Contracts: The 3-Year vs 4-Year Dilemma

So, you're in the market for a shiny new Audi A1 Sportback and weighing up the options between a 3-year and a 4-year Personal Contract Purchase (PCP) agreement. It's a common quandary, especially when you're looking at attractive finance rates like Audi Solutions Finance at 6.8%, and you've got a healthy £4,000 deposit ready to go. The core question often boils down to how to balance those desirable lower monthly payments with the overall cost and flexibility of the deal. Let's delve into the nuances of each option to help you make an informed decision.

Understanding PCP Fundamentals

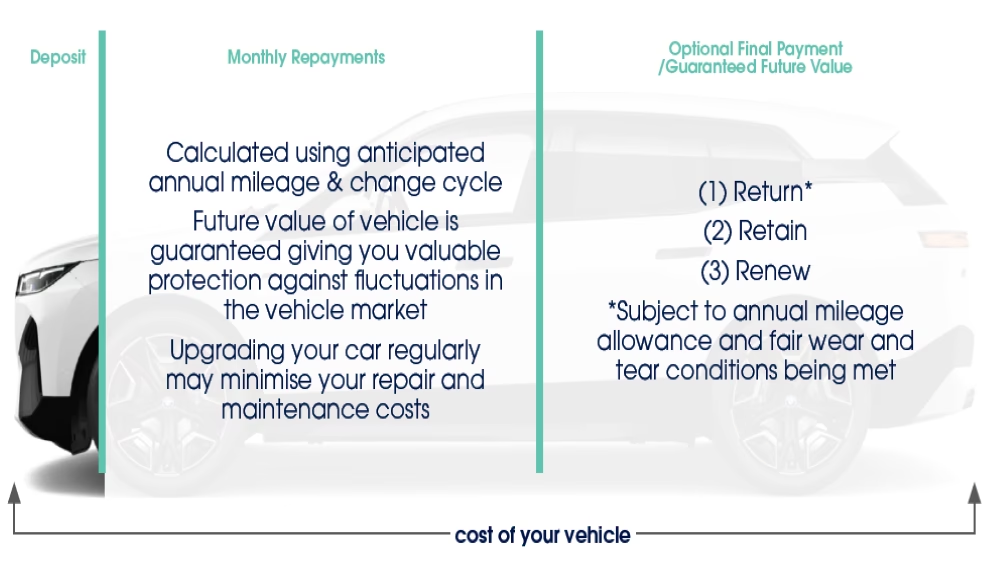

Before we dive into the specifics of your Audi A1, it's crucial to grasp how PCP works. A PCP agreement essentially finances the difference between the car's initial price and its Guaranteed Future Value (GFV) – the predicted value of the car at the end of your contract. You make monthly payments on this difference, along with interest, and at the end of the term, you have three options: pay the GFV to own the car outright, hand the car back (provided you've met mileage and condition stipulations), or part-exchange it for a new vehicle, using any equity towards a new purchase.

The 3-Year Contract: Pros and Cons

Opting for a 3-year PCP contract on your Audi A1 Sportback will generally result in higher monthly payments compared to a 4-year deal, assuming all other factors (deposit, mileage, interest rate) remain the same. This is because you're compressing the depreciation and financing costs over a shorter period.

Advantages of a 3-Year Contract:

- Lower Mileage Incurred: Typically, a 3-year contract will mean you've driven fewer miles than on a 4-year contract, assuming you're sticking to a similar annual mileage allowance. This can mean the car is in better condition at the end of the term.

- Earlier Upgrade Potential: You'll be eligible to upgrade to a new car sooner. This is appealing if you like to drive the latest models or if your needs might change within three years.

- Less Depreciation Risk: While the GFV is guaranteed, the longer you keep a car, the more it depreciates in real terms. A shorter contract means you're exposed to less of this longer-term depreciation.

- Potentially Higher Equity: If the car performs better than the GFV predicts, you might have more equity to put towards your next vehicle.

Disadvantages of a 3-Year Contract:

- Higher Monthly Payments: This is the most significant drawback. Your monthly outgoings will be higher, which might strain your budget.

- Less Financial Flexibility: With higher payments, you have less disposable income each month.

The 4-Year Contract: Pros and Cons

A 4-year PCP contract will spread the cost over a longer period, leading to lower monthly payments. This makes a new Audi A1 more accessible from a monthly budgeting perspective. You mentioned that the GFV only depreciates by £1,000 between year three and year four, which is a key piece of information.

Advantages of a 4-Year Contract:

- Lower Monthly Payments: This is the primary attraction. Making your car more affordable on a month-to-month basis is a significant benefit for many buyers.

- Increased Financial Flexibility: Lower monthly payments free up more of your budget for other expenses or savings.

- Potentially Lower Overall Interest Paid (in some scenarios): While you're paying interest for longer, the principal amount being financed each month is lower, which can sometimes lead to a lower total interest charge over the life of the loan, depending on how the GFV is structured. However, this is not always the case and needs careful calculation.

- Benefit from Lower Depreciation in Later Years: As you've noted, the depreciation rate often slows down in the later years of a car's life. Capturing that slower depreciation in your GFV for year four could be financially advantageous if you intend to keep the car beyond the contract term or if you're aiming for higher equity at the end of the 3-year mark.

Disadvantages of a 4-Year Contract:

- Higher Total Cost of Finance: You will be paying interest for an extra year, which will increase the total amount of interest paid over the life of the contract.

- Greater Depreciation Risk: You are exposed to the car's depreciation for an additional year. While the GFV protects you from the worst-case scenario, the actual market value could fall more significantly over four years than over three.

- Car Will Be Older at End of Contract: At the end of a 4-year contract, your Audi A1 will be four years old. This might mean it's closer to needing more significant maintenance and repairs, and it might not feel as 'new' as it would after only three years.

- Lower Equity Potential: Because the car is older and has depreciated for longer, the equity you have at the end of a 4-year contract is likely to be lower than at the end of a 3-year contract, especially if you plan to use that equity for a new car.

Analysing Your Specific Situation

You've highlighted a crucial point: the GFV difference between year three and year four is only £1,000. This is a significant factor. Let's break down what this means:

- Scenario 1: 3-Year Contract. If you opt for a 3-year contract, you'll pay more each month, but at the end of three years, the car's GFV will be £1,000 higher than if you had chosen a 4-year contract. This means your final payment (the balloon payment) will be £1,000 higher.

- Scenario 2: 4-Year Contract. With a 4-year contract, your monthly payments are lower. However, at the end of the contract, you'll have paid an extra year's worth of interest, and the balloon payment will be £1,000 less than the 3-year option.

The £1,000 Depreciation Factor: The fact that depreciation slows down significantly in the fourth year is good news for your GFV. However, you need to consider what you're paying in interest over that fourth year. If the interest you pay in that extra year is more than £1,000, then keeping the car for the full four years is financially less appealing than potentially ending the 3-year contract and using the higher GFV to your advantage (e.g., part-exchanging for a new car with less outstanding finance).

Making the Choice: Key Considerations

To help you decide, ask yourself these questions:

- What is your priority: Lower monthly payments or a lower final balloon payment? If budget is tight, the 4-year deal is attractive. If you prefer to have more equity or a higher resale value at the end of the term, the 3-year deal might be better.

- How long do you realistically plan to keep the car? If you know you'll want a new car in three years, the 3-year contract aligns perfectly. If you're open to keeping it longer, the 4-year contract might be considered, but be aware of the increased age and potential maintenance costs.

- What is the total interest cost for each option? This is crucial. Get a full breakdown from Audi Solutions Finance for both the 3-year and 4-year terms. Compare the total interest paid.

- What is your expected annual mileage? Ensure the mileage allowance in both contracts is sufficient for your needs. Exceeding it can incur significant charges, which could negate the benefits of lower monthly payments.

- How important is driving a relatively new car? A 3-year-old car is generally in better condition and more modern than a 4-year-old car.

Hypothetical Comparison Table

Let's imagine a simplified scenario to illustrate the financial impact. (Note: these are illustrative figures and may not reflect your exact offer).

| Feature | 3-Year Contract | 4-Year Contract |

|---|---|---|

| Monthly Payment | £350 | £300 |

| Total Monthly Payments (3 years) | £12,600 | £10,800 |

| GFV (End of Year 3) | £16,000 | £15,000 |

| Balloon Payment (End of Year 3) | £16,000 | £15,000 |

| Total Paid to Year 3 (Excl. Deposit) | £12,600 | £10,800 |

| GFV (End of Year 4) | N/A | £15,000 |

| Monthly Payment (Year 4) | N/A | £300 |

| Total Monthly Payments (4 years) | N/A | £14,400 |

| Balloon Payment (End of Year 4) | N/A | £15,000 |

| Total Paid to Year 4 (Excl. Deposit) | N/A | £14,400 |

| Difference in Total Paid (Year 4 vs Year 3) | £0 | £1,800 |

| Difference in GFV (Year 4 vs Year 3) | £1,000 higher GFV | £1,000 lower GFV |

In this example, the 4-year deal saves you £200 per month (£2,400 per year) but costs an extra £1,800 over the four years compared to three years of payments on the 3-year deal. Crucially, the GFV is £1,000 lower at the end of the 4-year contract. This means that to get out of the 4-year contract and have the car paid off, you're paying £1,800 in extra monthly payments plus an extra £1,000 in the balloon payment, totalling £2,800 more compared to the 3-year option, but you've had lower monthly payments for an extra year. This highlights the importance of total cost.

Frequently Asked Questions

Q1: What if I want to change my car after 2 years?

A1: With a PCP, you can usually part-exchange your car before the contract ends. However, you'll need to settle the outstanding finance, which will include the remaining monthly payments and a portion of the GFV. You'll only have equity if the car's market value is higher than the outstanding finance amount. Shorter contracts might leave you with less equity if you exit early.

Q2: What are the implications for my credit score?

A2: Taking out any finance agreement will involve a credit check. The duration of the contract itself usually has minimal direct impact on your credit score, but managing payments responsibly is key. A longer contract means a longer period of credit commitment.

Q3: Is the GFV guaranteed even if the car market crashes?

A3: Yes, the GFV is guaranteed by the finance company. If the car's market value falls below the GFV, you can hand it back without owing any more (provided you haven't exceeded mileage or damaged the car). You will, however, lose your deposit and any payments made.

Q4: Can I make overpayments on a PCP?

A4: Generally, you cannot make overpayments to reduce the monthly payments on a PCP. You can sometimes pay off the outstanding finance early, but this usually means paying the GFV plus any remaining interest, which may not be financially beneficial.

Conclusion: Which is Right for You?

Your decision hinges on your financial priorities and how long you envision keeping the Audi A1. The £1,000 difference in GFV between year three and year four is a critical piece of data. If the interest you'd pay in that fourth year significantly outweighs this £1,000 GFV benefit, then the 3-year contract might be more prudent for future flexibility and potentially a higher equity position when you next change your car.

However, if the immediate relief of lower monthly payments is paramount, and you're comfortable with the car being older at the end of the term, then the 4-year contract offers that accessibility. Always request a full breakdown of the total interest payable for both options. Understanding the total cost of finance is often more revealing than just looking at the monthly payment or the GFV alone. Good luck with your Audi purchase!

If you want to read more articles similar to PCP Deals: 3 vs 4 Year Contracts, you can visit the Automotive category.